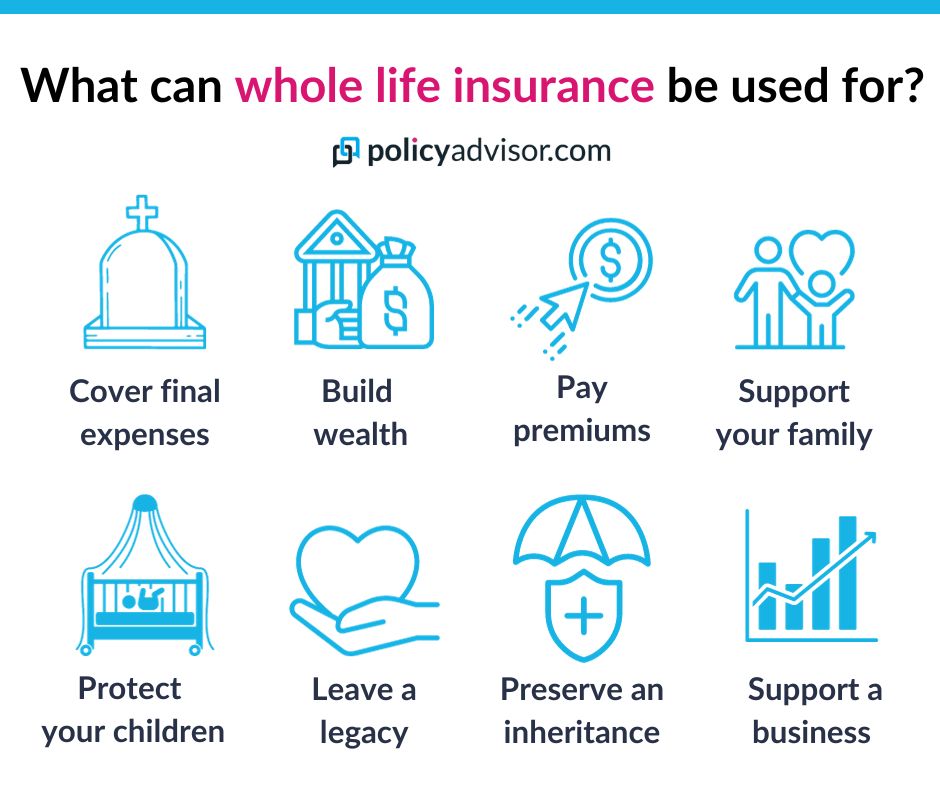

Understanding Whole Life Insurance: How It Functions as an Unfunded Retirement Plan

Whole life insurance is often misunderstood, yet it serves a unique purpose that can be highly beneficial as an unfunded retirement plan. Unlike traditional retirement accounts that rely on contributions to grow funds, whole life policies accumulate cash value over time, which policyholders can borrow against or withdraw. This cash value is separate from the face value of the policy, allowing individuals to access funds without the need for a taxable event, making it a versatile tool for financial planning.

To effectively utilize whole life insurance as an unfunded retirement plan, it's essential to understand its key components. First, the premium payments contribute to both the death benefit and the cash value. Second, the cash value grows at a guaranteed rate, providing a stable return over the long term. Finally, policyholders can use the cash value in various ways, such as supplementing retirement income, funding major purchases, or addressing unforeseen expenses. By integrating whole life insurance into your financial strategy, you can create a safety net that not only serves your heirs but also contributes to your financial security during retirement.

The Benefits of Whole Life Insurance: A Hidden Asset for Your Retirement

Whole life insurance is often overlooked as a key component of retirement planning, but its benefits extend far beyond just providing a death benefit. This type of insurance accumulates cash value over time, which can serve as a significant financial resource during your retirement years. Unlike term life insurance, which expires without any financial return, whole life policies build a hidden asset that can be accessed via loans or withdrawals. This means that as you approach retirement, you can tap into this cash value to supplement other income sources, helping to ensure a more comfortable lifestyle.

Additionally, the premiums you pay for whole life insurance contribute to a stable and predictable investment. Unlike more volatile investment options, the cash value grows at a guaranteed rate established by the insurer. This makes whole life insurance a reliable component of a diversified retirement strategy. By incorporating it into your financial planning, you not only secure a safety net for your beneficiaries but also create an asset that can appreciate over time, providing peace of mind and financial security as you enter your golden years.

Does Whole Life Insurance Really Serve as a Retirement Strategy?

Whole life insurance is often marketed as a multifaceted financial tool, combining the benefits of life coverage with a cash value component. Many individuals consider it as a potential retirement strategy due to its ability to accumulate cash value over time. Unlike term life insurance, which provides coverage for a specific period, whole life insurance offers lifelong coverage and the possibility of growing savings that can be accessed during retirement years. However, it’s essential to analyze if its advantages outweigh its costs, as premiums can be significantly higher than those for term policies.

Using whole life insurance as a retirement strategy may appeal to those seeking a conservative approach to their financial planning. The cash value can serve as a source of funds for emergencies or supplemental income once the policyholder reaches retirement age. Furthermore, the death benefit can provide financial security to beneficiaries. That said, potential policyholders should carefully evaluate their long-term financial goals and consider alternatives such as IRAs or 401(k) plans, which may offer higher returns without the complexities associated with life insurance policies.